GAM Explains: SFDR

This article explains the EU’s Sustainable Finance Disclosure Regulation (SFDR) in a technical and detailed format.

Click here for PDF version.

For a quick summary, you can skip to our top takeaways section, which tells you the three main points we think you should know about this important piece of sustainable finance regulation, and the overview box for a summary of requirements.

- What is it?

- Why it matters to investors

- Three top takeaways

- What to look out for

Introduction

The SFDR has been law in European Union (EU) Member States since 10 March 2021, with subsequent implementation deadlines throughout 2022, 2023 and 2024. Introduced by the European Commission (EC) alongside the Taxonomy Regulation, the SFDR forms part of a package of legislative measures within the EU’s sustainable finance strategy.

Its main aims are:

- to support investors to make more informed decisions regarding the sustainability characteristics of their investments

- to assess how sustainability risks are integrated into investment decisions

- ultimately to contribute to attractive private capital to support Europe’s net zero and sustainability goals.

Since it was first introduced, markets within and outside the EU have developed additional guidance, taxonomies and proposed labelling regimes. In September 2023, the EC launched a consultation to assess the implementation of the SFDR framework. The EC sought to understand implementation challenges and potential limitations as well as exploring possible options to improve the framework. Further to this the European Securities and Markets Authority (ESMA), published its final report with proposed amendments to the Regulatory Technical Standards (RTS).

Here we look at the main features of SFDR and highlight the areas where it may develop.

What is it?

The SFDR introduced standardised disclosures for market participants. The scope of the SFDR includes financial advisers that provide investment advice, and participants in financial markets producing or selling financial goods and portfolio management services. The regulation applies to firms based in the EU; however its scope includes investment managers or advisers outside of the EU who advise, or seek to market, products to European customers.

The impact of this regulation is far-reaching. Required disclosures cover a firm’s sustainability practices and specific product level disclosures.

Why it matters to investors

The SFDR helps investors make better informed and more sustainable choices, with its main purpose to provide greater transparency on environmental and social characteristics and improve consideration of sustainability factors within investment decisions.

The regulation also seeks to boost transparency from the product level disclosure requirements, in particular those focused on principal adverse impacts (PAIs) and taxonomy alignment have added on additional drivers for corporate disclosure on these issues. There are, however, often data gaps, especially for companies that have not been required to report sustainability-related metrics. The introduction of the Corporate Sustainability Reporting Directive (CSRD) should further support better data quality and consistency.

Ultimately the SFDR aims to re-orientate capital flows to finance the transition to a more sustainable economy, addressing systemic risks such as climate change, nature loss and inequality.

Three top takeaways

1) SFDR is about disclosure, not labelling

The SFDR categories represent levels of disclosures that a fund will make. There are clear parameters but currently no minimum thresholds or specific requirements on environmental or social characteristics, or a definitive definition of what constitutes a sustainable investment. Currently one of the challenges of the SFDR is that it is insufficiently clear on some key terms which makes it difficult for consistent interpretation across firms. With this uncertainty, we have seen certain funds change their classifications; for example in the final quarter of 2022, when Morningstar analysis showed 40% of funds were shifted from Article 9 to Article 8. While uncertainty remains, there is likely to be continued flux.

2) SFDR aims to level the playing field

The SFDR is not a standalone piece of regulation, and on top of helping investors to make informed decisions, stands to provide greater comparability for users. The framework aims to work in concert with the EU taxonomy and EU climate benchmarks to create strong sign-posting and stronger market incentivisation for more sustainability aware investment.

3) Further changes should be expected

Two key drivers of this are the EC consultation and the ESMA final report with proposed amendments to the RTS, both of which we discuss below.

What to look out for

The dust has far from settled on the final agreements of the SFDR. In September 2023 the EC released a three-month consultation which aimed to understand how the SFDR has been implemented and review key concerns. The EC consultation included a set of questions for respondents to identify how they aligned with them, and appeared to raise the prospect of further developments for SFDR, including:

1) Potential creation of a categorisation system for financial products: As expected, the consultation sought to address the issue of Article 8 and Article 9 being used as de facto labels. To address this, the consultation explored potential options for how to develop a more precise EU-level product categorisation system. Two main options were put forward:

a. build on the current distinction between Article 8 and Article 9 products, to convert these into formal product categories.

b. develop an approach focusing on the type of investment strategy, based on different criteria and concepts (such as removing the distinction between Articles 8 and 9 from the disclosure framework). The categories proposed within the consultation have some overlap with the proposed labels of the Sustainability Disclosure Requirements (SDR) in the UK and, depending on the outcome of the consultation, this could indicate the future trajectory of the SFDR.

2) Potential changes to entity level requirements: The consultation asked the question whether “the SFDR [was] the right place to include entity-level disclosures” and in the context of other EU reporting frameworks, “to what extent is there room for streamlining sustainability-related entity-level requirements across different pieces of legislation?”. This could indicate that the EC is considering the usefulness of entity-level disclosures, and whether potential changes are needed to these disclosures. If entity level disclosures were removed, alternative disclosure requirements could fall under other regulatory frameworks such as the CSRD or the Capital Requirements Regulations.

3) Interaction with other regimes: With other markets and regimes, such as the Sustainability Disclosure Requirements (SDR) in the UK outlining product label categories, investors are mindful of the challenges of international interoperability. At present, the SFDR and the Sustainability Disclosure Standards (SDS) are far from being aligned and although this could change based on the outcome of the consultation, firms should consider carefully the reporting requirements they may fall under.

Separate from this broader consultation of SFDR, in December 2023 the ESA published its final report with proposed amendments to the RTS and the EC will decide on whether to endorse the proposals within the next three months.

These changes could have implications for firms reporting under the SFDR, albeit when they would impact is yet to be clarified.

The proposed amendments introduced by the ESA include:

- Changes to PAI indicators. This would see the addition of mandatory social and voluntary PAI indicators, and amendments and additional data points for existing PAIs.

- New detailed disclosures for financial products which have greenhouse gas (GHG) emissions reduction targets.

- A new dashboard for a simple summary of key information.

- Enhanced disclosure of how sustainable investments comply with the Do No Significant Harm principle.

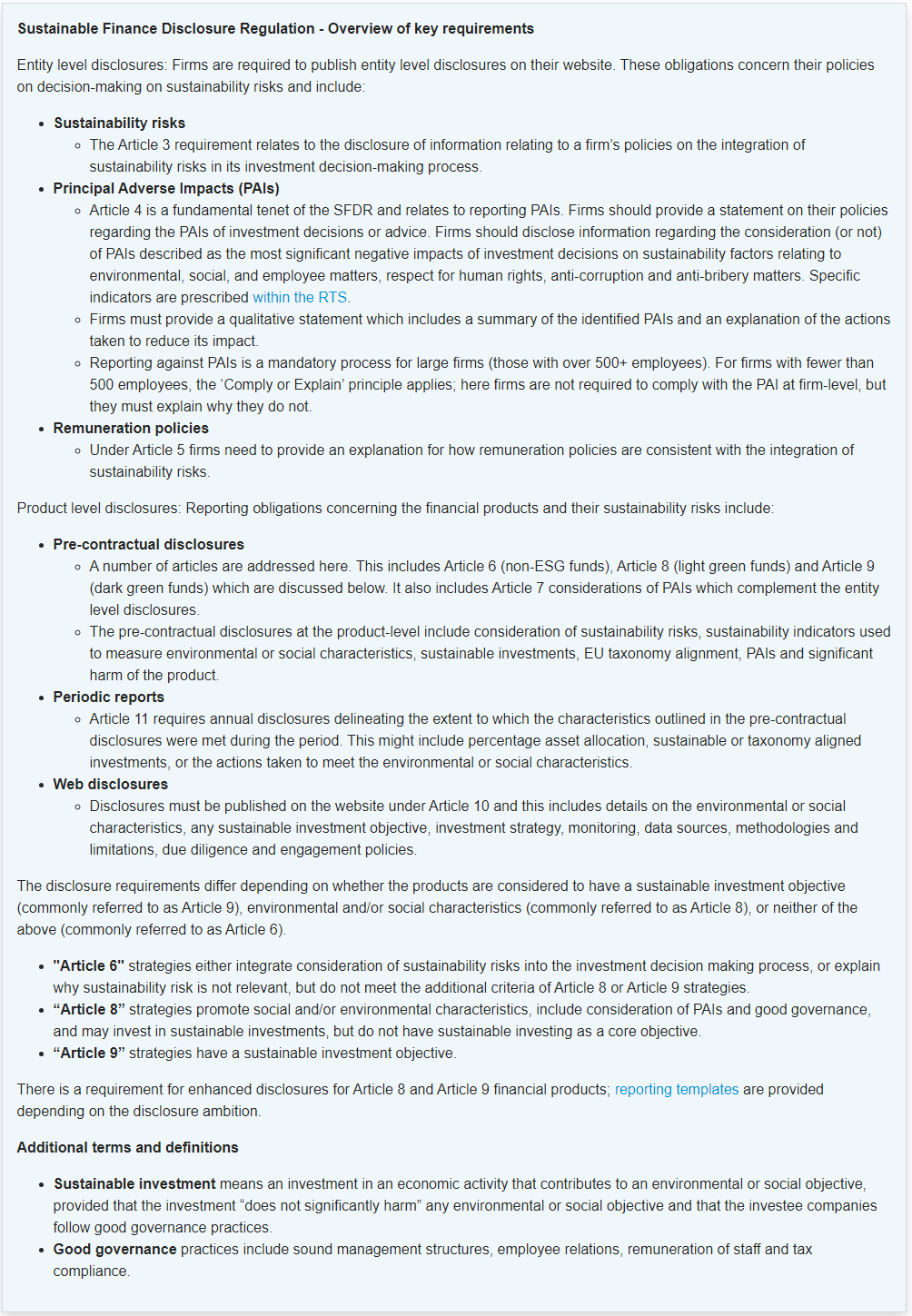

Click on image below to zoom in to read.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is not a reliable indicator of future results or current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented and are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee that forecasts will be realised.